Home › FX Trading School › Advanced

Market-Regime Detection & Adaptive Systems

Market-regime detection is the discipline of identifying which behavioural state a market is currently in — trending, ranging, or volatile/chaotic — so that a systematic strategy can adjust its parameters or stand aside rather than apply a one-size-fits-all rule to conditions it wasn't built for. This is Module 16 of the PipTax FX Trading School, and it assumes you've already worked through Module 12 (backtesting and walk-forward validation) and Module 14 (position sizing and risk-of-ruin). If either of those feels shaky, go back before continuing — regime work sits on top of a system that's already been honestly tested, not underneath one.

Everything here is about building more robust process, not about finding an edge that removes risk. No filter, however clever, turns a losing system into a guaranteed winner, and most retail accounts still lose money over time regardless of the tools used.

Why market-regime detection matters for systematic traders

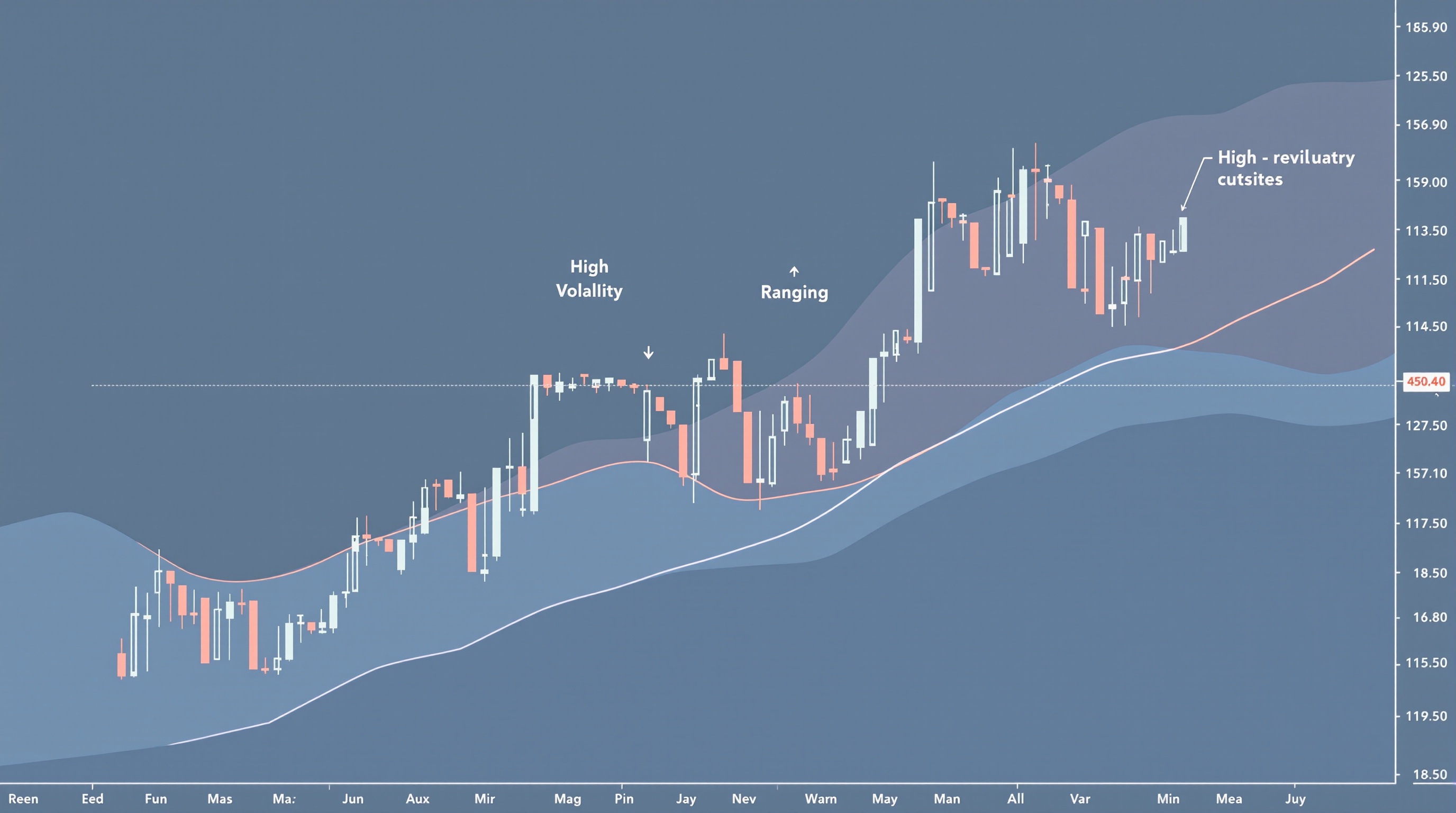

A single fixed rule set — say, a moving-average crossover — will look brilliant in a strong trend and dreadful in a choppy range. Traders who backtest over one regime and deploy live into another are often shocked when performance collapses, not because the market "changed" in some mysterious way, but because it moved into a state the strategy was never designed to handle.

Regime detection matters because:

- Trend-following systems typically need sustained directional moves to overcome whipsaw losses and cost drag.

- Mean-reversion systems need bounded, range-bound price action and tend to bleed in strong trends.

- Volatility-based sizing (stops, targets, position size) becomes miscalibrated when realised volatility shifts sharply.

- Cost sensitivity changes by regime — a strategy that trades frequently in quiet ranges is far more exposed to spread and commission drag than one that trades rarely in strong trends, which is exactly why cost modelling (see /cost-impact.html) has to be regime-aware, not a single blended average.

The goal isn't prediction of the future regime — it's honest classification of the present one, quickly enough to act.

Classifying regimes: the three practical states

Most workable frameworks reduce to three states, even though real markets are messier:

1. Trending — sustained directional movement with higher highs/higher lows (or the reverse), moderate to strong autocorrelation in returns. 2. Ranging/mean-reverting — price oscillating within a band, low directional persistence, negative short-term autocorrelation. 3. High-volatility/transitional — often around news events, session overlaps, or regime changes themselves; characterised by expanding ranges and unstable statistics.

Common classification tools, used individually or combined:

- ADX (Average Directional Index) — above ~25 often flagged as trending, below ~20 as ranging (thresholds are illustrative, not gospel).

- ATR (Average True Range) relative to its own longer-term average — rising ATR signals expansion/transition.

- Rolling autocorrelation of returns — positive suggests trend persistence, negative suggests mean reversion.

- Hurst exponent — above 0.5 trending, below 0.5 mean-reverting (computationally heavier, more academic).

- Simple structural rules — e.g., price relative to a slow moving average plus a volatility band (Bollinger-style) as a quick, transparent classifier.

Simplicity has a genuine advantage here: a transparent two-indicator classifier you fully understand beats a black-box model you can't explain when it fails.

Building an adaptive system: three levels of adaptation

Once you can classify regimes, you have three broad ways to build an adaptive trading system, increasing in complexity and fragility:

| Level | What adapts | Complexity | Overfitting risk | |---|---|---|---| | 1. Filter | Trade/don't trade based on regime | Low | Low | | 2. Parameter switch | Use different parameter sets per regime | Medium | Medium | | 3. Strategy switch | Run entirely different strategies per regime | High | High |

Level 1 (filter) is the most robust starting point: keep your existing trend-following logic, but only allow entries when ADX confirms trending conditions. This alone often removes a meaningful chunk of chop-related losses.

Level 2 (parameter switch) widens stops and targets in high-ATR regimes, tightens them in low-ATR regimes, and adjusts position size accordingly (tying directly back to Module 14's risk-of-ruin maths).

Level 3 (strategy switch) runs a trend system in trending regimes and a mean-reversion system in ranging regimes. This is powerful in theory but dangerous in practice because you're now backtesting two strategies plus a classifier — three sources of overfitting instead of one.

Building the classifier without overfitting it

The classifier itself is a model, and models can be overfit just as easily as entry rules. Guard against this by:

- Using out-of-sample validation on the classifier separately from the strategy, exactly as taught in the backtesting module.

- Preferring fewer, well-understood inputs over a stack of correlated indicators that all say roughly the same thing.

- Testing threshold sensitivity — if ADX 24 works but ADX 26 destroys the result, the classifier is fragile, not skilful.

- Checking regime persistence — regimes should last long enough (days to weeks in most FX timeframes) that the classifier isn't flipping state every few bars, which just adds noise and transaction costs.

- Logging regime transitions separately from trade signals, so you can audit whether losses cluster around transition periods (they often do).

A classifier that can't survive walk-forward testing on its own is not ready to gate a live strategy.

Practical workflow: from detection to execution

A workable end-to-end process looks like this:

1. Define regime states and the indicator(s) that classify them, in writing, before touching live capital. 2. Backtest the base strategy unconditionally, then again filtered by regime, comparing results honestly (Module 12 methods apply directly here — see /methodology.html for how PipTax approaches this kind of comparison). 3. Stress-test cost assumptions per regime using the cost tool at /audit.html, since trade frequency and holding time often differ by regime, changing your effective cost drag. 4. Paper-trade the adaptive version for a meaningful sample before going live, watching specifically for classifier lag at transitions. 5. Monitor live regime state alongside your equity curve, so a drawdown can be diagnosed as "wrong regime call" versus "strategy genuinely broken."

On execution, broker choice interacts with regime work in a practical way: a trend system that only fires occasionally is less sensitive to spread than a mean-reversion system firing dozens of times a week in a quiet range. Compare execution venues — for example Pepperstone's MetaTrader server offerings versus IG's own platform — for the specific instruments and regimes you intend to trade, using live figures from /brokers/index.html rather than assumptions.

Common pitfalls in market-regime detection

Watch for these recurring mistakes:

- Regime hindsight bias — labelling regimes with the benefit of full-sample data, then acting surprised the classifier "worked" in-sample.

- Too many regimes — splitting into five or six finely-tuned states usually just means more parameters to overfit.

- Ignoring transaction costs at transitions — switching strategies or standing aside still involves closing and reopening positions, which carries real cost (/rates.html has current swap and rollover context relevant here).

- Treating the classifier as infallible — it's a probabilistic label, not a fact; build in tolerance for misclassification.

- No kill switch — if the classifier itself starts behaving erratically (rapid flipping, extreme readings), the system should default to flat, not to guessing.

Conclusion: market-regime detection as a discipline, not a shortcut

Market-regime detection is genuinely useful systematic design work, but it's an extension of good testing discipline, not a way around it — every classifier and every adaptive layer needs the same walk-forward rigour you'd apply to a standalone strategy. Keep it simple, validate it honestly, and always model your real trading costs by regime rather than assuming an average that applies everywhere. Trading remains risky regardless of how adaptive your system is, and no regime filter changes that fact.

Key takeaways

- Market-regime detection classifies current conditions (trending, ranging, volatile) — it doesn't predict future price direction

- Start with simple, transparent filters (e.g. ADX thresholds) before attempting full strategy-switching systems, which carry much higher overfitting risk

- Every regime classifier needs its own out-of-sample validation, using the same walk-forward discipline taught for standalone strategies

- Trading costs often vary by regime because trade frequency and holding time differ — model this per regime via the cost tool rather than assuming one blended average

- Log regime transitions separately from trade signals so drawdowns can be diagnosed as classifier lag versus genuine strategy failure

- Adaptive systems reduce exposure to unsuitable conditions but do not eliminate risk — most retail accounts still lose money over time

Frequently asked questions

- Is market-regime detection the same as market prediction?

- No. Regime detection classifies the current state of the market (trending, ranging, volatile) using recent price behaviour. It doesn't forecast future direction — it simply tells you what conditions you're likely trading in right now, so your system can respond appropriately.

- What's the simplest way to start with regime filters?

- Add a single filter to an existing, already-tested strategy — for example, only taking trend-following signals when ADX is above a threshold. This is Level 1 adaptation: low complexity, low overfitting risk, and easy to backtest cleanly.

- Can regime detection remove drawdowns entirely?

- No. It can reduce exposure to conditions your strategy handles badly, but misclassification, transition periods, and genuine strategy risk remain. Trading is inherently risky and adaptive systems don't eliminate that.

- How many regimes should a system realistically use?

- Most robust systems use two or three (trending, ranging, and sometimes a volatile/transitional state). Adding more regimes usually increases overfitting risk faster than it adds genuine predictive value.

- Does regime affect trading costs?

- Yes — trade frequency and holding periods often differ by regime, which changes your exposure to spread, commission and swap. Model this per regime using the cost tool at /audit.html rather than relying on a single blended cost assumption.

- What prerequisite modules should I complete before this one?

- Module 12 (backtesting and walk-forward validation) and Module 14 (position sizing and risk-of-ruin) are assumed knowledge. Regime detection builds directly on both.